The Demand Side:

Now, don't get me wrong, in the event of a worldwide economic downturn, then, of course, oil prices will be coming down due to the fall in demand. However, we have to consider the possibility that this is just a temporary slowdown - the Fed is likely to be getting ahead of the US weakness on Wednesday when it is expected to cut rates by 25 basis points. Furthermore, the ECB is changing the structure of interest rates through the use of tiering. Finally, China is pumping a large quantity of stimulus into the economy which has helped to stave off a wider economic downturn.

So, for now, let's assume that the Federal Reserve is capable of engineering a "soft-landing".

|

| Source: https://www.reviewecon.com/money-market2/money-market-increase-supply1 |

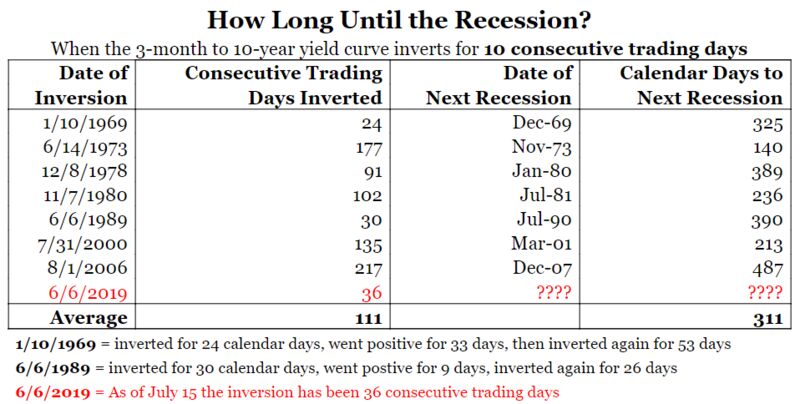

I know that many people believe the inversion of the yield curve is a recessionary indicator and has been very effective at predicting recessions historically. However, we must remember that the expansion following the financial crisis has not been "normal". Massive monetary stimulus has been pumped into the economy all around the world, and a basic understanding of the law of supply when we look at the money market can show that interest rates will be lower.

So, personally, I am not entirely convinced that this inversion of the yield curve will, in fact, lead to a recession since we are in uncharted waters.

Thus, I believe the expansion can continue for now. And thus, the demand concern is overstated.

So that covers the demand side for oil.

The Supply Side:

Over the last couple of weeks, we have been bombarded with headlines regarding Iran and its aggressions towards the Western World. Yet, we have not really noticed these events being priced into the market fully.

Below is a chart of the oil market and I have marked on the upswings which have occurred from data recently. What we see is that every upswing is marked by a move back to the downside. Yes, oil did end the week up over the previous trading week, but only marginally, and the swings to the downside always seemed far more aggressive than the gentle grinds upwards.

I have to say the big drop caught me quite by surprise and I was stung pretty heavily for a fairly large amount of money. But what has interested me about crude this week is the fact that we basically started and finished in exactly the same place, despite some major changes with regards to potential future supply.

Thus, this adds to my case that I believe the market is overpricing the downside risk.

Technically on the longer term....

I have to say that I literally just tried drawing these two trend lines on the weekly chart and it does look like there is something potentially in this trade with the narrowing range. Obviously, this could continue for several more weeks before we see a breakout either side, but it did strike me as interesting and a potential indicator that a major oil swing could be about to happen. Obviously though, we continue to be driven by fundamentals in this market.

So there we are, that's my two cents on the oil market and I hope people have found this analysis somewhat useful. Let me know if you have any ideas regarding oil, but my thesis for the month remains that we continue to trade in a similar range between $54 and $58 a barrel. With a longer term upside potential, dependent upon the outcome of the Fed's exercise in giving the market what it wants despite the economic data being bullish....

I mean engineering a soft landing!

Brexit means brexit

ReplyDeleteIndeed it does. There will be a more comprehensive GBPUSD Analysis released this weekend; explaining in detail the route the Brexit negotiations could now take.

Delete